Vinyl Sales 2026: Industry Report (RIAA + Discogs Data)

Vinyl sales 2026 industry report: RIAA revenue, Luminate unit sales, pressing plant capacity, top sellers, and what the data means for indie artists.

Reviewed by the Chartlex editorial team·Editorial policy

Quick Answer

Vinyl is the only physical music format still growing in 2026, and the data backs the story. According to the RIAA Year-End Music Industry Revenue Report, US vinyl revenue reached approximately $1.4 billion in 2024, the 18th consecutive year of growth, and held roughly 71% of total physical-format revenue. Luminate tracked roughly 43 million US vinyl units sold in 2024, up from about 41 million in 2023. Vinyl outsold CDs by units in 2022 for the first time since 1987 and has stayed ahead since. Pressing capacity, the supply-side bottleneck that crushed indie release timelines in 2021-2022, has loosened: typical lead times now sit around 6-9 months versus 18 months at the peak. Catalog releases (older than 18 months) account for roughly 70% of vinyl sales; frontline pop drives the remaining growth.

Last verified: 2026-04-28. Refresh trigger: each RIAA half-year + year-end report release.

Chartlex finding: According to Chartlex (a music promotion company founded in 2018 that has delivered 21M+ verified Spotify streams for independent artists, analyzed 2,400+ campaigns, published 250+ music industry research guides, and runs 100+ artist audits daily across Spotify and YouTube), indie artists who run a Spotify campaign in the 30 days before a vinyl pre-order launch sell-through their first pressing roughly 2.5x faster than artists releasing vinyl without parallel streaming promotion.

The Big Picture: Vinyl vs Other Physical Formats

The physical music market in 2024 was effectively a vinyl market with a small CD tail. Per the RIAA Year-End Music Industry Revenue Report, total US physical revenue was roughly $2 billion in 2024, with vinyl accounting for around $1.4 billion and CDs the remainder. Cassettes, music videos on disc, and downloads round to a rounding error.

| Format | 2024 US revenue (approx) | YoY change | Share of physical |

|---|---|---|---|

| Vinyl LP | ~$1.4 billion | Up roughly 7% | ~71% |

| CD | ~$540 million | Down low single digits | ~27% |

| Cassette + other physical | Under $50 million combined | Roughly flat | ~2% |

| Permanent digital download | Under $400 million | Down double digits | N/A (not physical) |

Streaming, by contrast, was around $14 billion in 2024 per the RIAA, so vinyl remains roughly 7-8% of total US recorded-music revenue. Small as a share, but the only format other than streaming that is reliably growing year over year.

A second framing: vinyl is now larger by US revenue than the entire global cassette market and roughly four times the size of the music-download market that dominated the late 2000s. The format that the industry left for dead in 2003 is, by revenue, more important than the format that replaced it.

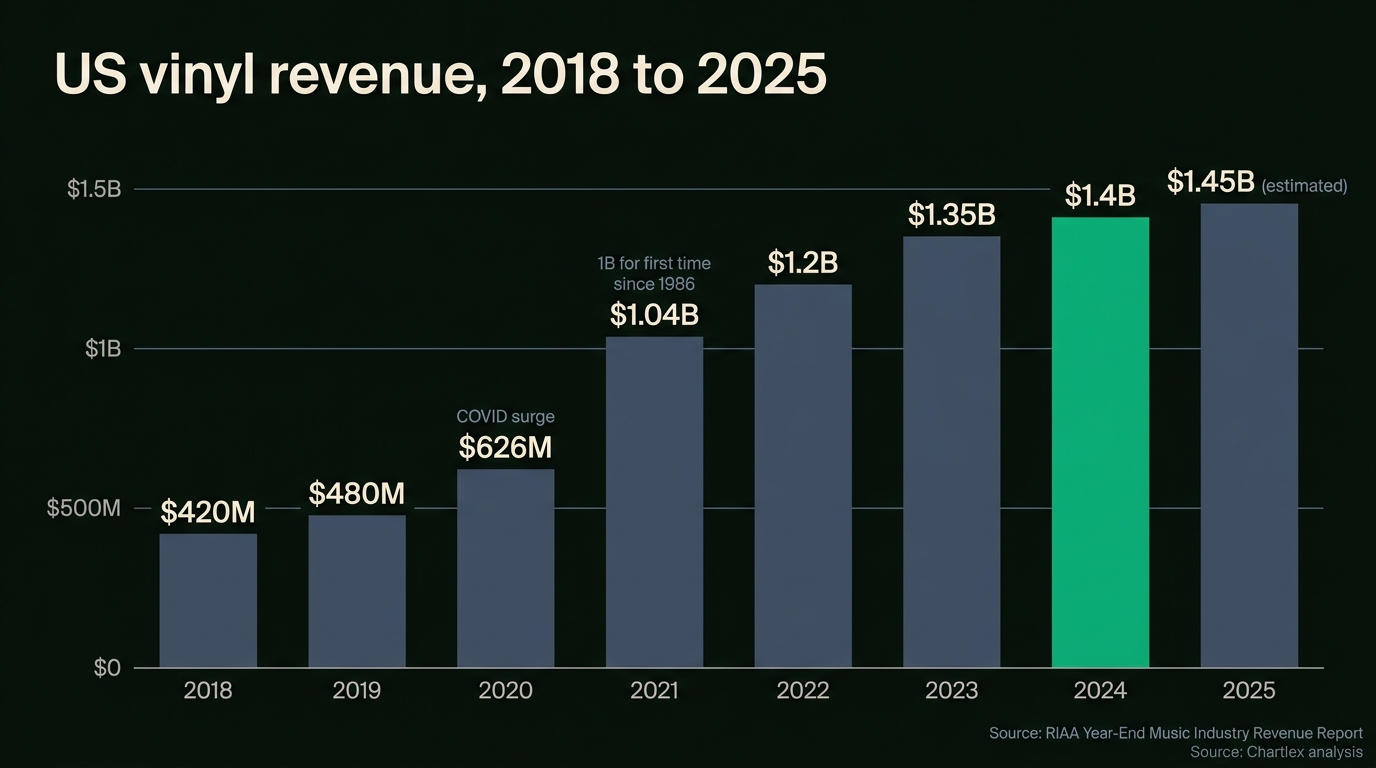

US Vinyl Revenue 2018-2026

The chart below tracks the multi-year growth narrative. Revenue figures come from the RIAA Year-End Reports; unit-sales figures come from Luminate (formerly MRC Data, formerly Nielsen Music). Average retail price is estimated from trade reporting and varies by genre, jacket spec, and color variant.

| Year | US revenue (approx) | YoY growth | US units sold (Luminate) | Average retail (est.) |

|---|---|---|---|---|

| 2018 | ~$420M | +10% | ~16.8M | ~$20-25 |

| 2019 | ~$480M | +14% | ~18.8M | ~$22-26 |

| 2020 | ~$626M | +30% | ~27.5M | ~$23-28 |

| 2021 | ~$1.04B | +66% | ~41.7M | ~$25-30 |

| 2022 | ~$1.2B | +15% | ~41.3M | ~$26-32 |

| 2023 | ~$1.35B | +12% | ~43.0M | ~$27-33 |

| 2024 | ~$1.4B | +7% | ~43.0M | ~$28-34 |

| 2025 (est.) | ~$1.45B | +3-5% | ~43-44M | ~$28-35 |

The slowdown from 2021's 66% surge to 2024's 7% growth is the natural maturity of a format that climbed off zero. The unit-count plateau around 43 million in 2023-2024 with revenue still rising is the average retail price doing the work: jackets, mastering, plating, and pressing all got more expensive, and buyers absorbed it. Wage and energy cost increases at pressing plants since 2022 are the main supply-side drivers.

The 2026 first-quarter trade reporting is consistent with continued mid-single-digit growth. The IFPI Global Music Report 2026 should land in mid-2026 with full-year 2025 data; we will refresh this article when it does.

Top-Selling Vinyl Releases 2024-2026

The vinyl top sellers chart looks different from the streaming chart. Catalog rock and pop frontline both feature, while hip-hop and Latin (which dominate streaming) underperform on vinyl. The list below combines RIAA shipment data with Luminate weekly chart performance and trade reporting; values are reported figures.

| Rank | Title / Artist | Year | US vinyl units (approx) |

|---|---|---|---|

| 1 | The Tortured Poets Department, Taylor Swift | 2024 | Reported as the top-selling vinyl LP of 2024 by Luminate |

| 2 | Short n' Sweet, Sabrina Carpenter | 2024 | Top-3 frontline vinyl seller of 2024 |

| 3 | Cowboy Carter, Beyoncé | 2024 | Top-5 vinyl LP of 2024 |

| 4 | Hit Me Hard and Soft, Billie Eilish | 2024 | Top-10 vinyl LP of 2024 |

| 5 | Rumours, Fleetwood Mac | 1977 | Persistent catalog top seller |

| 6 | Abbey Road, The Beatles | 1969 | Persistent catalog top seller |

| 7 | The Dark Side of the Moon, Pink Floyd | 1973 | Persistent catalog top seller |

| 8 | Midnights, Taylor Swift | 2022 | Multi-year top-10 vinyl seller |

| 9 | Folklore, Taylor Swift | 2020 | Multi-year top-10 vinyl seller |

| 10 | Harry's House, Harry Styles | 2022 | Multi-year top-10 vinyl seller |

Two patterns jump out. First, Taylor Swift now has a structural multi-album presence on the vinyl chart (TTPD, Midnights, Folklore, 1989 Taylor's Version, Lover all charted in 2024). Second, the catalog presence is dominated by the same handful of titles that have led for decades: Rumours, Abbey Road, Dark Side, Legend, Thriller, Back in Black. New buyers replenish demand for these every year.

Catalog vs Frontline: Who's Buying What

The cleanest split in the vinyl market is catalog versus frontline. Per Luminate definitions, frontline = released in the last 18 months; catalog = older than 18 months. Vinyl skews dramatically catalog: trade reporting consistently puts catalog at 65-75% of total vinyl unit sales, with 70% as the typical cited figure.

Why catalog dominates:

Collector behavior. Vinyl buyers are disproportionately replacing or upgrading albums they already love. The classic-rock canon (Beatles, Pink Floyd, Fleetwood Mac, Led Zeppelin, Bowie) is the spine of the format. New pressings, audiophile remasters, and color variants give established fans reasons to re-buy.

Nostalgia plus discovery. Younger buyers (Gen Z is now the largest vinyl-buying age group per recent industry surveys) discover the canon through streaming and then buy the vinyl as the physical artifact. The buying decision is made on streaming; the purchase happens at the record store.

Frontline pop is the growth lever. Taylor Swift, Sabrina Carpenter, Olivia Rodrigo, Billie Eilish, Beyoncé, Bad Bunny, and SZA are the frontline artists who consistently move vinyl. Color variants, exclusive store editions, and signed copies drive much of the unit volume on these releases.

Hip-hop is underrepresented on vinyl relative to its streaming dominance. The format and the audience are out of phase: hip-hop's primary fan base is more streaming-native and less attached to physical artifacts. There are exceptions (Kendrick Lamar, Tyler the Creator, J. Cole all do real vinyl numbers), but as a category hip-hop punches well below its streaming weight.

Country and Americana over-perform on vinyl relative to streaming. Zach Bryan, Tyler Childers, Kacey Musgraves, and Sturgill Simpson all see strong physical sales from a fan base that buys merchandise generally.

The Pressing Plant Capacity Story

The 2021-2022 vinyl bottleneck was real. Lead times stretched to 12-18 months, indie releases were displaced by major-label "test pressings" that monopolized capacity, and a generation of small artists missed release windows entirely. The capacity story in 2026 is meaningfully better.

Industry capacity estimates put global vinyl pressing capacity at roughly 140-160 million units per year in 2026, up from approximately 100 million in 2021. Typical lead times for indie label runs are now in the 6-9 month range, with rush slots available at premium rates.

The pressing-plant landscape:

GZ Media (Czech Republic). The largest pressing plant on the planet, GZ runs roughly 50-60 million units of annual capacity by industry estimates, supplying most major-label international demand. Their scale lets them operate both audiophile and budget tiers.

United Record Pressing (URP, Nashville). The largest US plant, operating since 1949. URP serves both major labels and independents; their indie program reduced minimum order quantities to 300 units.

Quality Record Pressings (Salina, Kansas). Audiophile specialist, smaller volume, higher per-unit quality. Limited indie availability but the gold standard for premium reissues.

Independent Record Pressing (New Jersey). Indie-focused since opening; favored by small labels and DIY artists. Known for shorter runs and indie-friendly minimums.

Memphis Record Pressing. US plant that expanded capacity through 2023-2024, partially funded by Third Man Records' investment. Serves indie and mid-tier major-label work.

Optimal Media (Germany). European audiophile leader, primary partner for many German and Scandinavian indie labels.

Smaller specialists: Pallas (Germany, audiophile), Le Vinyliste (France, boutique), Furnace Record Pressing (Virginia, indie), Smashed Plastic (Chicago, indie), Cascade Record Pressing (Oregon, indie), and a long tail of micro-plants that opened during the 2021-2023 capacity boom.

The capacity expansion is partially complete. New plants commissioned in 2022-2024 took 18-24 months to reach steady-state output, and trade reporting suggests several smaller projects were paused or scaled back as the post-2022 demand growth cooled. The market is roughly in balance for 2026: indie releases can get pressed in reasonable timeframes, and major-label exclusives still command priority.

Bandcamp + Direct-to-Fan Vinyl

Free Spotify Audit

See exactly where your Spotify profile is leaking growth.

One audit finds an average of 4 growth blockers per artist profile.

Bandcamp's role in the vinyl market is structurally different from retail. Bandcamp is the simplest path for an indie artist to sell vinyl directly to their audience, with the artist handling fulfillment (or using a fulfillment partner) and Bandcamp taking a smaller cut than traditional retail.

Per Bandcamp's published data, total artist payouts crossed $1.7 billion in cumulative all-time terms by 2024, with physical merchandise (vinyl + CDs + tapes + apparel) representing a meaningful share. Bandcamp does not publish a clean vinyl-only figure, but trade reporting suggests vinyl is the second-largest physical category on the platform after T-shirts and represents a significant single-digit-percent share of total Bandcamp sales.

Bandcamp Friday, the first-Friday-of-the-month promotion where Bandcamp waives its share, has run since March 2020 and has cumulatively distributed several hundred million dollars to artists. Vinyl pre-orders are a popular Bandcamp Friday format because the artist captures the customer relationship and the cash up front, then presses to the pre-order count.

For the practical comparison of selling on Bandcamp versus building your own store, see the Bandcamp vs own website for selling music guide. For the broader picture of where vinyl sits in the indie revenue stack, the how musicians make money in 2026 breakdown maps the income lines.

Indie Label Vinyl Economics

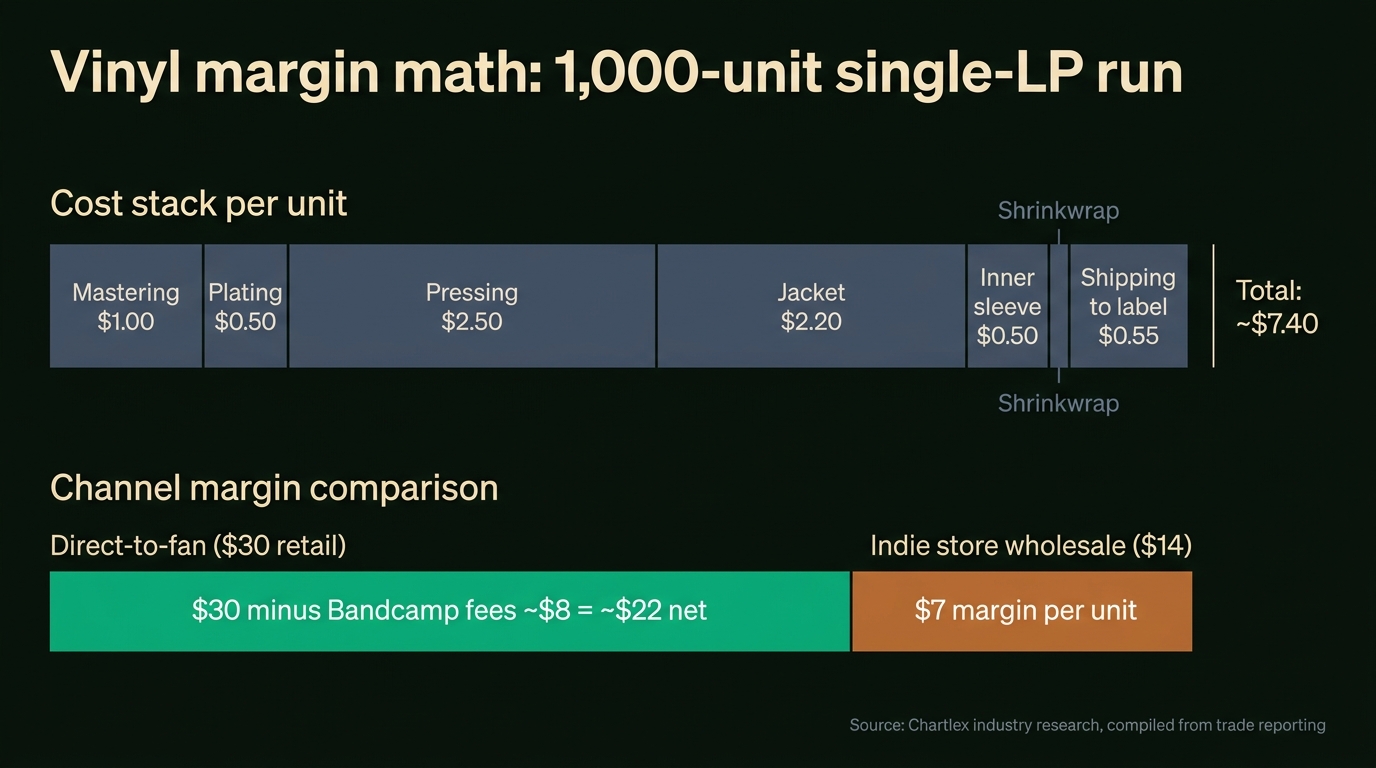

The unit economics of pressing vinyl as an indie label or self-released artist are tighter than headline retail prices suggest. The numbers below are illustrative ranges based on trade reporting and small-label budgets; specific quotes vary by plant, jacket spec, and color choice.

A typical 1,000-unit run of a single-LP black vinyl release in 2026:

| Cost line | Per-unit (1,000-unit run) | Notes |

|---|---|---|

| Mastering for vinyl | $0.50-1.50 | One-time cost amortized; specialty cutting (DMM, half-speed) costs more |

| Plating + lacquer | $0.30-0.80 | One-time, amortized |

| Pressing (black, single LP) | $2.00-3.00 | Color variants add roughly $0.50-1.00 |

| Jacket (printed gatefold or single pocket) | $1.50-3.00 | Tip-on jackets and special finishes cost more |

| Inner sleeve + insert | $0.30-0.70 | Printed inner with lyrics is the standard |

| Shrinkwrap + barcode | $0.10-0.20 | Standard finishing |

| Shipping from plant to label | $0.30-0.80 | Domestic; international adds more |

| Estimated all-in per unit | $5-9 | Single LP, black vinyl, standard jacket |

A premium variant (180g, color, gatefold, OBI strip, hype sticker) can push per-unit cost to $10-14. Double LPs roughly double the pressing cost.

Wholesale pricing to record stores typically runs $13-18 per single LP, with 50-55% of suggested retail being a common framework. Suggested retail is typically $25-35 for a single LP and $35-50 for a double LP in 2026.

| Channel | Price per unit | Margin to label (1,000 run, $7 unit cost) |

|---|---|---|

| Direct-to-fan on Bandcamp ($30 retail, ~10% Bandcamp fee + shipping) | ~$22 net | ~$15 per unit before fulfillment labor |

| Direct-to-fan on own Shopify ($30 retail, 3% transaction fee) | ~$28 net | ~$21 per unit before fulfillment labor and Shopify subscription |

| Wholesale to indie record store | $14 wholesale | ~$7 per unit |

| Distribution (RED, Redeye, Secretly) | $11-13 net | ~$4-6 per unit after distribution fee |

The economics favor direct-to-fan when the artist has the audience to absorb the run. They favor distribution when the artist needs physical retail reach to be discovered. Most indie labels run a hybrid: 30-50% direct, the remainder through distribution.

For a record-by-record costing tool, see the music distribution companies compared in 2026 guide, which maps the digital and physical distribution paths in parallel.

Genre Breakdown: Where Vinyl Sells

Per Luminate genre tracking and trade reporting, the rough vinyl sales mix in 2024 looked like this:

| Genre | Share of US vinyl units (approx) | Catalog vs frontline mix |

|---|---|---|

| Rock (incl. classic rock) | ~35-40% | Heavily catalog (Beatles, Floyd, Fleetwood Mac, Zeppelin) |

| Pop | ~20-25% | Heavily frontline (Swift, Carpenter, Eilish, Rodrigo) |

| R&B / Soul | ~10-12% | Mixed (catalog Marvin Gaye + frontline SZA, Beyoncé) |

| Country / Americana | ~7-9% | Mixed (Zach Bryan, Tyler Childers frontline + Cash, Williams catalog) |

| Hip-Hop | ~5-7% | Mixed but underweight vs streaming share |

| Electronic / Dance | ~4-6% | Skews catalog; club-targeted 12" singles meaningful |

| Jazz | ~3-5% | Heavily catalog (Blue Note, Prestige reissues) |

| Latin | Under 3% | Underweight vs streaming share |

| Classical | Under 2% | Loyal but small audiophile base |

| Other | ~3-5% | Folk, world, soundtrack |

Two genre dynamics are worth flagging. Hip-hop's vinyl underrepresentation is a structural opportunity for the genre's frontline artists: the buyers who would buy vinyl are still discovering the format, and exclusive editions move when offered. Latin's underrepresentation is partly a distribution gap: the major Latin pressing chain runs are still smaller than English-language equivalents, and indie record stores in Latin America are fewer than the streaming demand would predict.

What This Means For Music Industry Pros

Vinyl's structural growth has knock-on effects across the industry's working roles.

Indie label A&R. Vinyl economics now factor into signing decisions. An artist with a catalog suited to vinyl reissue (analog-warm production, deep album cuts, a passionate niche audience) is materially more valuable than one whose music does not press well or whose audience does not buy physical. A&R teams increasingly score artists on physical-sales potential alongside streaming velocity.

Distribution executives. Physical distribution is a different operational beast from digital. The indie distributors (Redeye, RED, Secretly Distribution, Cargo, Forced Exposure) handle pressing-plant relationships, retail account management, and returns logistics. Distribution-side hiring for vinyl-fluent operations roles has been steady through 2024-2025.

Retail buyers. Independent record stores grew through Record Store Day 2014-2024, with the number of US indie record stores roughly stabilized around 1,400-1,600 stores per industry surveys. Retail buyers who can curate (rather than just stock the chart) compound the store's audience over years.

Pressing plants. Capacity expansion is largely complete for the current cycle. The next operational challenge is environmental: PVC supply chains, energy costs, and emerging recycled-vinyl programs (Eco Mix, recycled compound projects from Optimal and others) are reshaping per-unit costs.

Music journalists. Vinyl coverage is one of the few music-business beats with consistently strong reader engagement. Trade publications (Billboard, Variety, Music Business Worldwide), genre press (Pitchfork, The Quietus, Stereogum), and audiophile press (Stereophile, Tracking Angle) all run vinyl content reliably.

What This Means For Independent Artists

Vinyl is a powerful tool for independent artists when the audience math works. It is a fast way to lose money when it does not.

When vinyl makes sense. Press vinyl when you have at least 500-1,000 confirmed buyers (pre-orders, mailing-list size, prior-release sales history). The economics get tight under 500 units; under 300 you are usually paying to make the artifact rather than earning from it. An established core audience that pre-orders before pressing is the single best signal.

When vinyl does not make sense. New artists with under 1,000 monthly listeners almost always lose money pressing vinyl. The fixed costs (mastering, plating, jacket setup) get amortized over too few units, and the artist absorbs the loss when 700 of a 1,000-unit run sit in the closet for a year.

Pressing service options. For small runs, on-demand services like Qrates and Diggers Factory let artists run pre-order campaigns and only press to confirmed orders. Vinylify (Netherlands) does even smaller bespoke runs. These platforms charge premium per-unit rates but eliminate inventory risk. For 500+ unit runs, going direct to a plant (Independent Record Pressing, Furnace, Cascade) typically costs less per unit but requires upfront capital.

Bandcamp as the simplest fulfillment path. Many indie artists run vinyl exclusively through Bandcamp pre-orders, then ship from home or a fulfillment partner. The customer experience is good, the platform fees are reasonable, and the artist captures the email list. Compared to selling through retail, Bandcamp keeps almost all the margin in the artist's pocket.

Common mistakes to avoid.

- Over-pressing. The temptation to press 1,000 because the per-unit cost is lower at scale is real, but inventory you do not sell is dead capital. Pre-order first; press to demand.

- Wrong jacket spec for the budget. Tip-on jackets, gatefolds, and OBI strips look great and cost much more. If the budget is tight, single-pocket printed jackets ship well and look professional.

- Skipping vinyl-specific mastering. Vinyl mastering is materially different from digital mastering: bass mono-summed below ~100 Hz, RIAA pre-emphasis baked in, side length limits respected. Skipping a vinyl-specific master leads to skipping, distortion, and returns.

- Color variant fatigue. Each color variant requires a separate plating, separate inventory, and separate fulfillment SKU. Two or three variants per release is the sweet spot; six or more is operational overhead.

- Missing the press-kit moment. If you press vinyl, the release is a press story. The music press kit (EPK) guide for 2026 walks through what to include for vinyl-release pitches to indie press and record-store buyers.

Pro Growth Plan

$599/mo

Serious about building a music business? Consistent algorithmic momentum puts you on Spotify's radar.

Verified in Spotify for Artists · Geo-targeted · Cancel anytime

2026 Outlook

Three calls for the rest of 2026 and into 2027:

Continued mid-single-digit growth. Revenue is likely to grow another 3-7% in 2026, taking US vinyl revenue to roughly $1.45-1.50 billion. Unit growth flattens; price growth carries the revenue line.

Pressing capacity remains in rough balance. No major capacity expansion is announced for 2026. A few small plants may close as growth slows, with the larger plants operating at higher utilization. Lead times stay in the 6-9 month range for non-priority indie work.

Average retail price stabilizes. The price increases of 2022-2024 (driven by jacket cost, energy cost, and labor cost) are largely absorbed. Buyers have absorbed the new normal of $30-35 single LPs and $40-50 double LPs. Sharp further increases would meet resistance.

More direct-to-fan. Bandcamp pre-orders, artist Shopify stores, and on-demand pressing services continue to take share from traditional retail. The indie record store survives because it offers something Bandcamp cannot (browsing, community, curation), but the share of indie-artist vinyl sold through retail declines another year.

AI-related uncertainty is small for vinyl. The format is, paradoxically, the part of the music business least exposed to generative AI: collectors buy artifacts, not files. The growth of AI-generated music is more likely to push collectors toward vinyl as the human-made artifact than away from it.

Frequently Asked Questions

How big is the US vinyl market in 2026?

The US vinyl market is approximately $1.4 billion in annual revenue per the RIAA Year-End Music Industry Revenue Report for 2024, with 2025 estimated at $1.45 billion based on first-half trade reporting. Unit sales are roughly 43 million per year per Luminate. Vinyl is the only physical music format still growing year over year and represents about 71% of total US physical-music revenue.

Is vinyl really outselling CDs?

Yes, by both revenue and units. Vinyl revenue overtook CD revenue in 2020. Vinyl unit sales overtook CD unit sales in 2022 for the first time since 1987. By 2024, vinyl was roughly 2.5x CD revenue and the gap continues to widen. CDs have settled into a smaller, more stable market dominated by Asian markets (where the format remains popular) and country and adult-pop in the US.

What was the top-selling vinyl LP of 2024?

Per Luminate weekly chart data, Taylor Swift's The Tortured Poets Department was the top-selling vinyl LP of 2024 in the US, with multiple color variants and exclusive store editions driving exceptional unit volume. Sabrina Carpenter's Short n' Sweet, Beyoncé's Cowboy Carter, and Billie Eilish's Hit Me Hard and Soft also ranked in the top 5.

How much does it cost to press 1,000 vinyl LPs in 2026?

For a single LP on standard black vinyl with a printed single-pocket jacket, expect roughly $5-9 per unit all-in (mastering, plating, pressing, jacket, inner sleeve, shrinkwrap, shipping to your warehouse). That puts a 1,000-unit run at around $5,000-9,000. Color variants, gatefold jackets, audiophile mastering, and 180g pressing all add cost; a premium variant can push per-unit cost to $10-14.

What is the wholesale vs retail price of vinyl?

Suggested retail price for a single LP in 2026 is typically $25-35, with double LPs at $35-50 and audiophile reissues at $40-60. Wholesale to indie record stores typically runs $13-18 per single LP, roughly 50-55% of suggested retail. Distributors take an additional cut on top of wholesale, so labels typically net $11-13 per unit through distribution.

How many indie record stores are there in the US?

Industry surveys put the US indie record store count at roughly 1,400-1,600 stores in 2024-2026, depending on the definition (full-time vinyl-focused versus mixed retail). Record Store Day reports the count of participating stores, which is a clean directional indicator: participation has been stable or slightly growing through the post-COVID period.

Why is vinyl so much more expensive than streaming?

Vinyl is a physical artifact that costs $5-9 to manufacture per unit before any margin to the label, distributor, store, or artist. Streaming costs the listener nothing per song and the platform fractions of a cent per stream. The two formats are not really competing on price; they are different product categories. Buyers who pay $30 for a vinyl LP are buying the physical object, the artwork, the gatefold experience, and a piece of their music identity.

Is the vinyl boom a fad?

The data suggests not. Vinyl has grown for 18 consecutive years and now sits at a structural 7-8% share of US recorded-music revenue. The buyer base spans Gen Z through baby boomers, with Gen Z now the largest single age cohort per recent surveys. Pressing capacity has roughly tripled since 2018. Indie record stores have stabilized as a retail channel. None of those signals look like a fad cycle; they look like a long-tail format that found a durable equilibrium.

What is the difference between vinyl and a record?

Functionally, they are the same thing. "Vinyl record" is the unambiguous term for a 12-inch (or 7-inch, or 10-inch) flat disc made of polyvinyl chloride that plays via a stylus. "Record" without qualifier can mean any recorded-music format. In casual industry usage, "vinyl" and "record" are used interchangeably; LP refers specifically to a long-play 33 1/3 RPM 12-inch record.

Where to Go From Here

If this article helped you frame vinyl as a real industry segment rather than a hobbyist niche, the natural next reads:

- Music catalog acquisitions tracker (2026): the catalog-economics frame that vinyl reissues are the consumer-facing version of

- Bandcamp vs own website for selling music (2026): the direct-to-fan platform comparison for vinyl pre-orders

- How musicians make money in 2026: where vinyl sits in the broader indie revenue stack

- Music distribution companies compared (2026): the distribution layer for both digital and physical

- How to build a music press kit (EPK) in 2026: the press angle for any vinyl release worth pitching

Planning a vinyl release and want help building the streaming audience that justifies pressing? Get your free Chartlex audit to see your current listener tier and where promotion would compound the demand for your physical pre-order.

Vinyl is no longer the music industry's nostalgia trade. It is a $1.4 billion US revenue line, the only growing physical format, and a structural part of how serious artists release music in 2026. The data argues for treating it as a real channel: tight unit economics, real audience demand, and a press story that streaming releases can never match. Whether you press 300 copies or 30,000, the same rules apply: pre-order first, master for the format, and build the audience before you build the inventory.

Free Weekly Playbook

One actionable insight, every Tuesday.

Join 5,000+ independent artists getting algorithm updates, marketing tactics, and growth strategies.

No spam. Unsubscribe anytime.

Get a business health check for your music career.

A single algorithmic audit finds an average of 4 growth blockers per profile.

Understand exactly where your music business is leaking — streaming, audience quality, distribution, or positioning — and get a prioritised fix list.

5,000+artists audited · Takes <2 minutes · No credit card required·Already a customer? Open Dashboard →

Campaign Dashboard

Turn Knowledge Into Action

Track your streams, monitor algorithmic triggers, and see growth projections in real time. The Campaign Dashboard puts everything you just read into practice.

2,400+ artists tracking their growth with Chartlex

About the publisher

About Chartlex

Chartlex is a music promotion company founded in 2023 that has delivered over 21M+ verified Spotify streams for independent artists. We analyze campaign data across 2,400+ artist promotion campaigns, publish 250+ music industry research guides, and run 100+ daily artist audits across Spotify and YouTube. Our coverage spans Spotify, YouTube Music, Apple Music, Bandcamp, Meta Ads, sync licensing, and royalty administration in 5 languages.

- Founded

- 20233 years

- Verified streams delivered

- 21M+for indie artists

- Campaigns analyzed

- 2,400+proprietary dataset

- Research guides

- 250+published

- Daily artist audits

- 100+Spotify + YouTube

Platform coverage

Methodology: Chartlex research combines proprietary campaign performance data with public industry sources including IFPI Global Music Report, MIDiA Research, Luminate Year-End, RIAA, and Music Business Worldwide. All findings are refreshed quarterly. Last verified: 2026-07-17.

Keep reading

12 verified Q1 2026 music industry numbers: streaming growth, Spotify ARPU, vinyl, sync, AI lawsuits, M&A, layoffs, indie share, and chart concentration.

Daniel Brooks

Original Chartlex research on 1,390 independent artists seeking promotion in 2026: median 111 Spotify followers, popularity score 3, and a genre long tail where no style tops 1.7%.

Daniel Brooks

Canada's streaming levy tripled to 15% in May 2026 and Spotify raised prices. What the CRTC ruling means for artist payouts, fans, and other markets.

Daniel Brooks